- Big tech earnings from the Magnificent 7 dominate the US earnings calendar

- US and Australian inflation reports to influence near-term rate expectations

- PMI reports will test US economic exceptionalism tag

- US Treasuries aren’t behaving like the ultimate safe haven asset

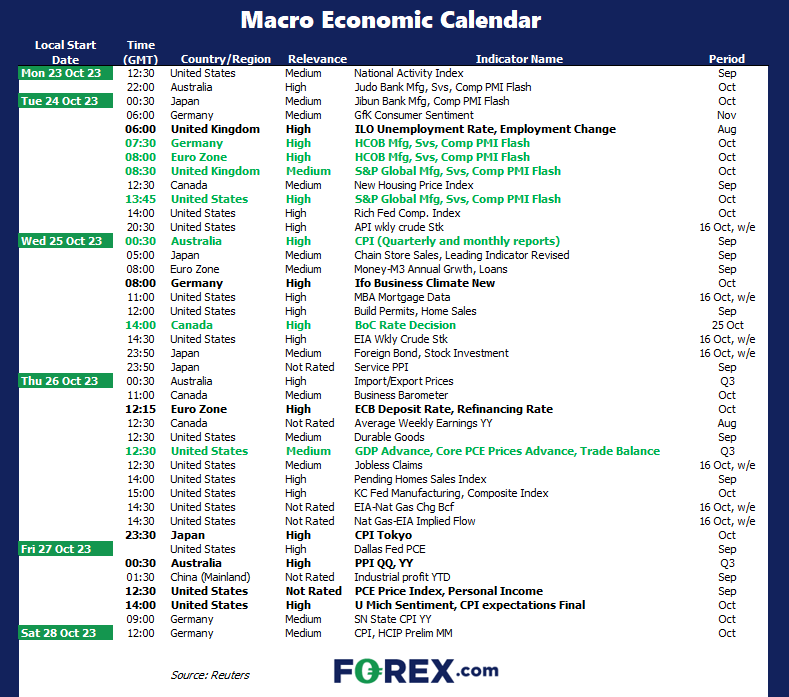

Following a volatile week characterised by geopolitical tension, an ongoing rout in US Treasuries and enough Fed speak to last a lifetime ahead the FOMC meeting blackout, the event risk picks up as we enter late October with big tech earnings, inflation reports from the US and Australia, rate decisions from the Eurozone and Canada and latest batch of PMI reports joining the mix, creating an environment that should provide ample opportunities for traders.

Earnings test for ‘Magnificent 7’ following Tesla crash

If surging bond yields globally weren’t enough for risk assets to contend with, we’re now about test the earnings metal from the very stocks that have kept the S&P 500 afloat this year, known widely as the ‘Magnificent 7’. As we saw with Tesla this week, in a market where so much excitement has been baked in when it comes to artificial intelligence and other future growth areas, and the apparent revenue riches they will bring, any disappointment in the near-term can and will be punished.

By the middle of the week we should have a good idea on how solid the foundations of the tech rally truly are. Microsoft and Alphabet arrive on Monday, followed by Meta a day later. Amazon reports on Thursday. Just to make things interesting, Visa, Verizon, Coca Cola, Dow, Mastercard, Boeing, Chevron and Exxon Mobil are also at bat.

With events in the bond market with geopolitical tensions ratcheting higher, you get the sense that it’s the bottom of the ninth, bases loaded with earnings having to knock it out of the park to stave off growing downside risks.

We have you covered with our earnings page here.

Core PCE inflation key to near-term Fed moves

Arriving at the tail end of the week is the Federal Reserve’s preferred measure of underlying price pressures, the core PCE deflator. It’s always important, but especially so in an environment where markets are growing increasingly uneasy about the Fed’s willingness to put the inflation genie to bed by suggesting higher bond yields are doing the work for them, resulting in bond yields and market-based inflation measures pushing noticeably higher.

Core PCE is seen lifting 0.2% for September following an 0.1% increase in August.

Australia CPI to confirm or dash RBA rate hike hopes

Out of the entire G10 FX universe, only Australia’s OIS curve has one full interest rate increase priced in. That means a lot will be riding on the outcome of Australia’s inflation report on Wednesday, especially following hawkish comments from the RBA in the minutes of its October monetary policy meeting.

Forget all the other previews; all that really matters from this event is what happens with the trimmed mean measures which strips out volatile items. It’s expected to increase by an uncomfortable 1.1% for the quarter, accelerating from the 0.9% pace of Q2. Just to make matters interesting, new RBA governor Michele Bullock will be speaking either side of the release on Tuesday and Thursday.

PMI Tuesday to test US economic exceptionalism story

Flash PMI reports from around the world will provide the latest snapshot on how activity levels are faring. Given the momentum being apparently carried by the US economy right now, markets will be particularly attentive to what the report for October has to say, especially the services sector given its importance to the broader economy.

Here’s the full weekly calendar to see what’s going on in your neck of the trading woods.

Scutty’s view

US Treasuries are behaving like a risk asset rather than safe haven, signaling we may be entering unchartered territory on how investors will respond to episodes of market turmoil in the future.

Buy bullion, bonds and buck whenever dark clouds gather on the horizon. It’s been a proven strategy for decades, providing shelter against capital losses. Given the situation in the Middle East, after the most aggressive monetary policy tightening episode in decades, we’ve now arrived at such a moment. The dark clouds are no longer in the distance but sitting right above us.

Gold has responded how you would expect. Same too the US dollar. But rather than being the ultimate safe haven, providing deep liquidity and security, US Treasuries are getting hosed, selling off when they would normally be bid. Given the implications for asset valuations globally, this should concern every investor.

Ask yourself the question: if US bonds can’t rally in this environment, when will they?

Given the unsustainable fiscal trajectory, gridlocked Congress and rupturing geopolitical landscape, it’s not surprising investors are baulking. The risks are obvious; hence they’re demanding ever higher compensation.

What we do know is that during the inflation-targeting era, two and 10-year yields have matched or exceeded the midpoint of Fed funds target range on every occasion. If that pattern repeats, it suggests benchmark yields could see another 35-40 basis points uplift beyond what’s already been seen. Given the way notes are trading right now, it could easily be higher.

Have markets adjusted for this vastly different environment? That’s something for you to ponder, but I seriously doubt it.

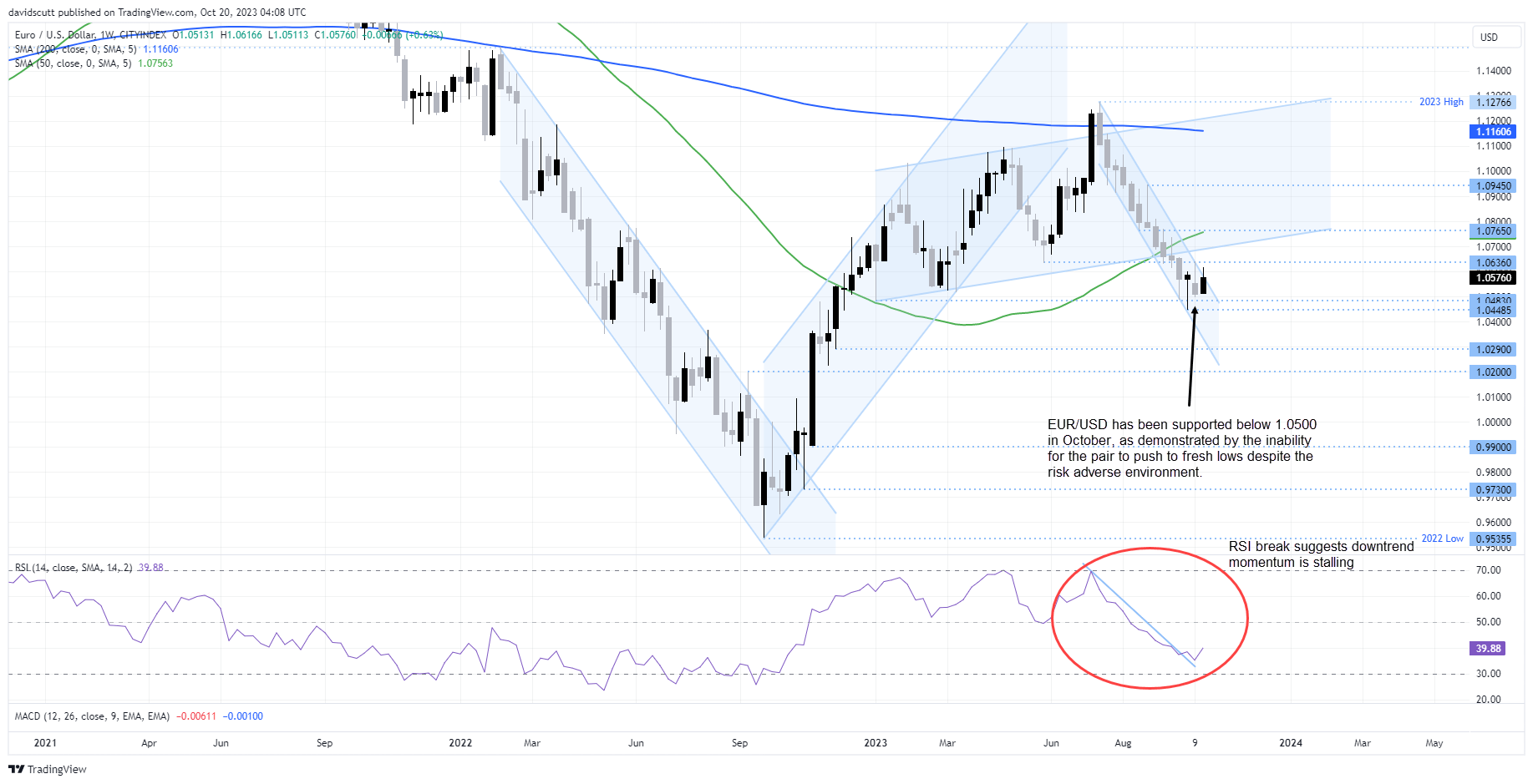

Market of the week: EUR/USD

Given the US dollar is the undisputed global reserve currency, how it performs impacts just about everything in markets. Given its significant weighting it has in the US dollar index, you could therefore argue the euro isn’t too far behind when it comes to significance.

Even with the increase in uncertainty generate by the conflict between Israel and Hamas, something has really stood out in the FX universe of late: the USD hasn’t found a substantial bid, in part due to resilience in the euro.

Looking at the EUR/USD weekly, a ding-dong battle is underway with sellers and buyers attempting to outdo each other by forcing the pair out of the channel it’s been stuck in since July. Like a tennis match between two baseline sluggers, the price has gone back-and-forth without really going anywhere.

A hammer followed by an inverted hammer in the prior two weeks suggests buyers won’t let further downside come easily having watched the pair fall to 2023 lows earlier this month. With the current weekly candle indicating buyers are winning the battle, and RSI suggesting downward momentum is ebbing, a potential for a break of channel resistance appears to be growing, at least from what the technicals are suggesting.

A channel break targets sees upside resistance at 1.0636 and 1.0765. Alternatively, another rejection of channel resistance opens the for a potential retest of support at 1.0480 and again around 1.0450.

-- Written by David Scutt

Follow David on Twitter @scutty

Latest market news

Today 02:05 PM

Today 11:59 AM

Latest articles

Today 11:59 AM

November 29, 2024 12:43 PM

November 28, 2024 10:58 PM