With FX traders once again focused on US political developments (to say nothing of the kickoff of the biennial Ryder Cup), the loonie has quietly snuck to the top of the major currency pack today.

Canada’s currency found some support after OPEC concluded its weekend meeting without formally recommending an increase in oil production. A Reuters report yesterday stated that Saudi Arabia would temporarily pump an additional 500,000 barrels per day to offset aggressive American sanctions against Iran, but this decision is merely a token gesture to appease an irate President Trump, who demanded that OPEC pump more to bring prices lower.

Ultimately, on planet that consumes more than 100 million barrels of oil per day, a temporary 0.5M increase is not likely to move the needle for oil prices. As a result, we’ve seen Brent crude oil prices climb to their highest levels in four years, hitting a high above 83.00 today. Because oil is Canada’s most important export, we’ve seen the loonie catch a bid sympathy.

Meanwhile, this morning’s Canadian data was also solid, with July’s GDP reading printing at 0.2% m/m, a tick better than the 0.1% increase expected. This marks the fifth time in the past six months that Canada’s GDP reading has come in above economists’ expectations and makes it highly likely that the BOC will raise interest rates next month.

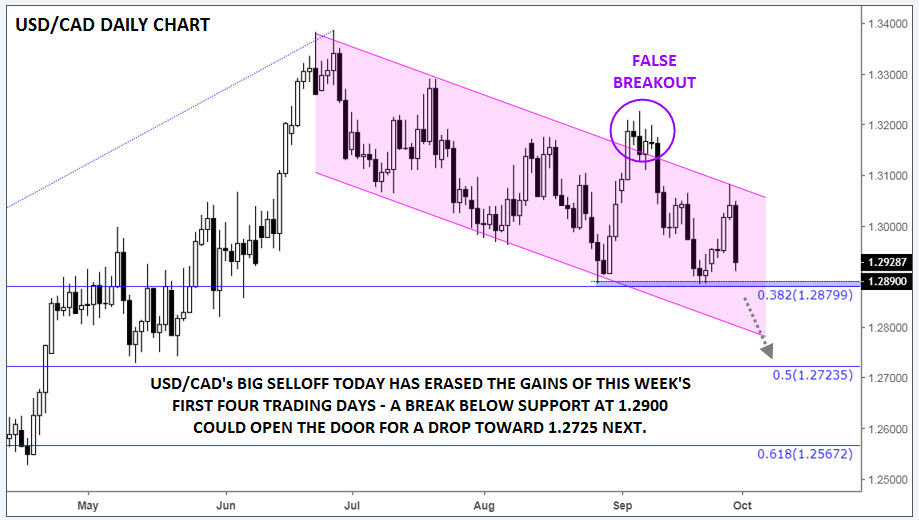

Technically speaking, USD/CAD has returned to test a key support level around the 1.2900 handle. After seeing a false breakout from its bearish channel off the late June high earlier this month, the pair dropped down to test this level for the first time late last week.

The early week recovery off that floor has been completely erased by today’s big bearish day, leaving no doubt where the current momentum lies. A break below 1.2900 could expose the 50% Fibonacci retracement near 1.2725 in time, whereas only a break above this week’s high would shift the near-term bias back to neutral.

Source: TradingView, FOREX.com

Latest market news

Today 02:05 PM

Today 11:59 AM

Latest articles

October 23, 2024 02:57 PM

July 1, 2024 03:53 AM

June 5, 2024 05:25 AM

May 20, 2024 04:04 AM