In a world where financial media sensationalizes every US jobs report as “The Most Important Jobs Report Ever,” even the most bombastic personalities had to admit today’s release was relatively insignificant, at least as far as Non-Farm Payroll reports go.

After all, the US economy had shown job growth for 94 consecutive months heading into today, and the Federal Reserve has seemingly already decided to raise interest rates at its meeting later this month. And, with three more NFP reports scheduled before the Fed’s next “live” meeting in December, today’s report alone was never likely to have any substantial impact on monetary policy…which is unfortunate for Fed hawks, because this morning’s jobs report finally showed signs of the wage acceleration that the central bank has been waiting on for nearly a decade.

On a headline basis, the BLS estimates that the US economy created 201k jobs in August, slightly above economists’ expectations of +190k new jobs. That said, the previous two reports were revised lower to show -50k fewer jobs were created and the unemployment rate held steady at 3.9%, so the overall quantity of jobs created were a slight disappointment. However, improvement the quality of the jobs was enough to offset those concerns.

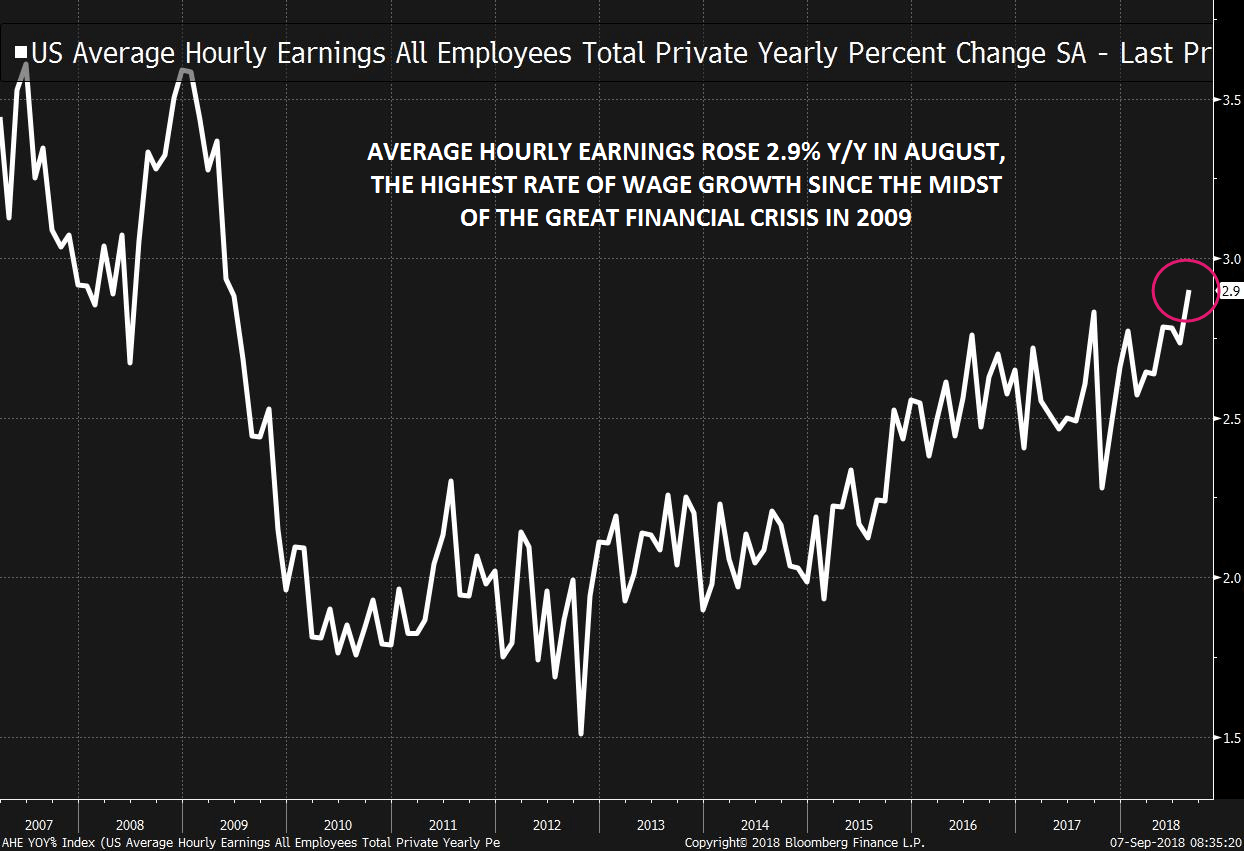

Specifically, average hourly earnings rose by 2.9% year-over-year (0.4% month-over-month), the highest reading since the midst of the Great Financial Crisis in 2009. Meanwhile, average hours worked held steady at 34.5 hours/week, suggesting that US consumers truly are putting more money in their pockets. It is worth noting that the Labor Force Participation Rate, or the percentage of US citizens either employed or actively seeking employment, ticked down 0.2% to 62.7%, so the potential for higher wages isn’t (yet) pulling discouraged job seekers off the sidelines.

As we noted above, this solid jobs report comes at a fairly “low impact” time in terms of its policy impact. The Fed, as widely telegraphed, will raise interest rates by 25bps later this month, a move that has already been completely “priced in” to the markets. The more interesting question is “What does today’s report mean for the December Fed meeting?” At the margin, it seems to make it more likely the central bank will raise interest rates for the fourth time this year, with the market-implied odds of a rate hike ticking up from 73% to 76% according to the CME’s FedWatch tool. Traders are (wisely, in your humble author’s opinion) waiting to see whether today’s strong wage growth figures are maintained in the coming months – to say nothing of the geopolitical and trade risks looming – before concluding that the labor market has finally turned the corner to accelerating wage growth.

Source: Bloomberg, FOREX.com

Market Reaction

Markets are acting as expected for a report that increases the odds of another interest rate increase this year. The benchmark 10-year Treasury bond is rising 5bps to yield 2.93% while US stock indices are falling by about 0.5% on the open, give or take. Meanwhile, the US dollar index is bouncing back above the 95.00 level, with the greenback gaining ground against all of its major rivals except sterling, which is rallying on the back of some positive Brexit rhetoric.

Latest market news

Today 02:05 PM

Today 11:59 AM

Latest articles

October 31, 2024 01:30 PM

February 1, 2024 04:02 PM

March 22, 2023 09:38 AM

January 24, 2023 07:42 AM