- Last week came across as a game-changer for USD/JPY directional risks

- US interest rate outlook remains key to USD/JPY movements

- Fedspeak, Treasury auctions, US CPI key event risks ahead

- USD/JPY biased higher but easy money from longs has likely been made

Overview

USD/JPY is likely to take its cues from US bond yields this week, putting speeches from Federal Reserve officials, Treasury auctions and key consumer price inflation data firmly in the drivers’ seat. The only obvious exception to the rule would be a major escalation or de-escalation of tensions in the Middle East, an outcome that is incredibly difficult to predict.

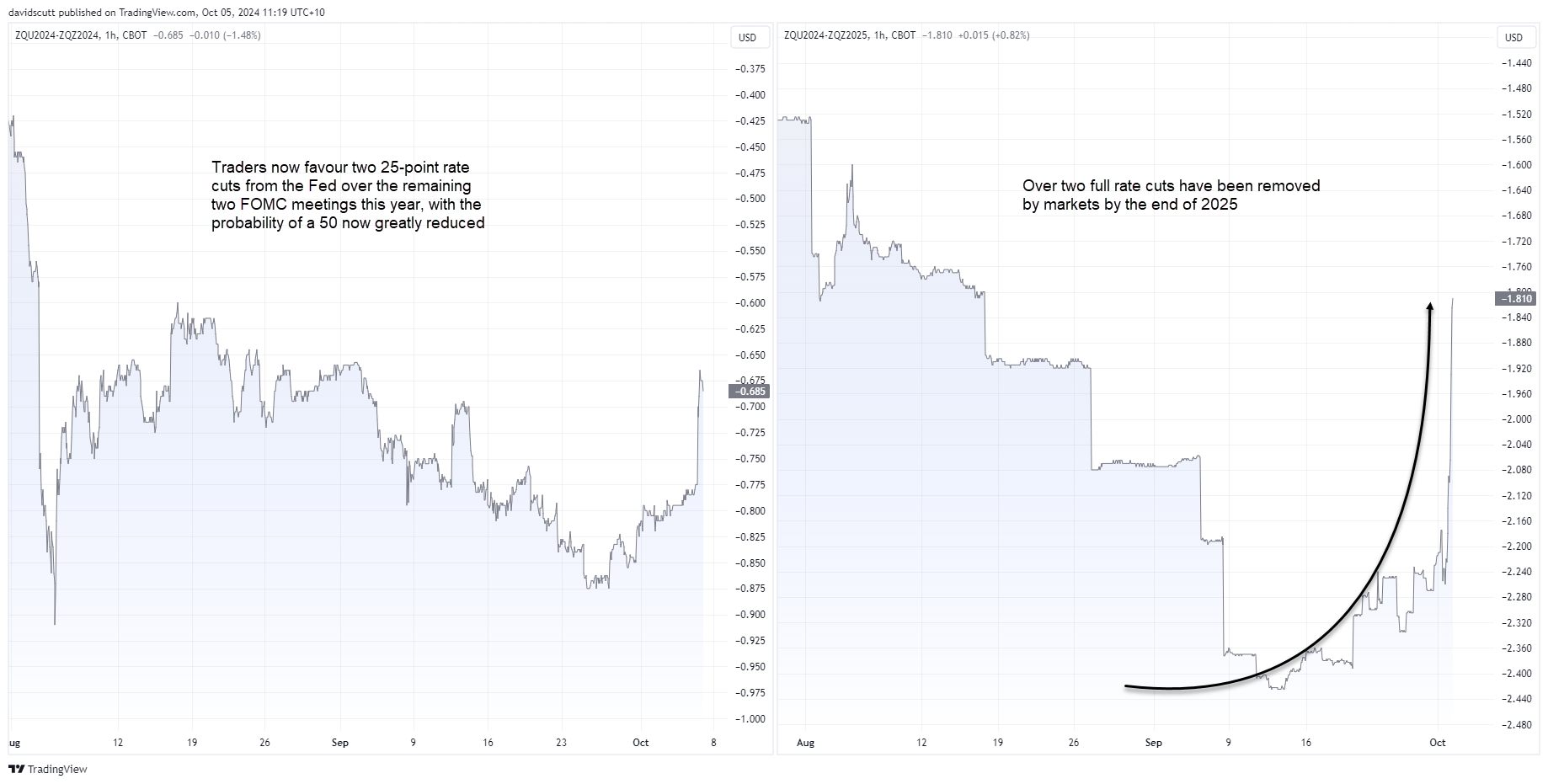

Fed rate cut pricing slashed

Last Friday’s blowout non-farm payrolls report changed the conversation regarding the outlook for US interest rates, seeing the debate shift from whether the Federal Reserve will cut the funds rate by 50 or 25 basis points next month to whether it will cut rates at all? It was as strong a report for this point in the cycle as you could wish for, with robust hiring, reduced unemployment and underemployment and firm wage pressures.

You can see the impact it had on Fed rate cut pricing in the chart below, especially expectations on the scale of easing expected by the end of 2025 which has tumbled by more than 60 basis points from the recent highs.

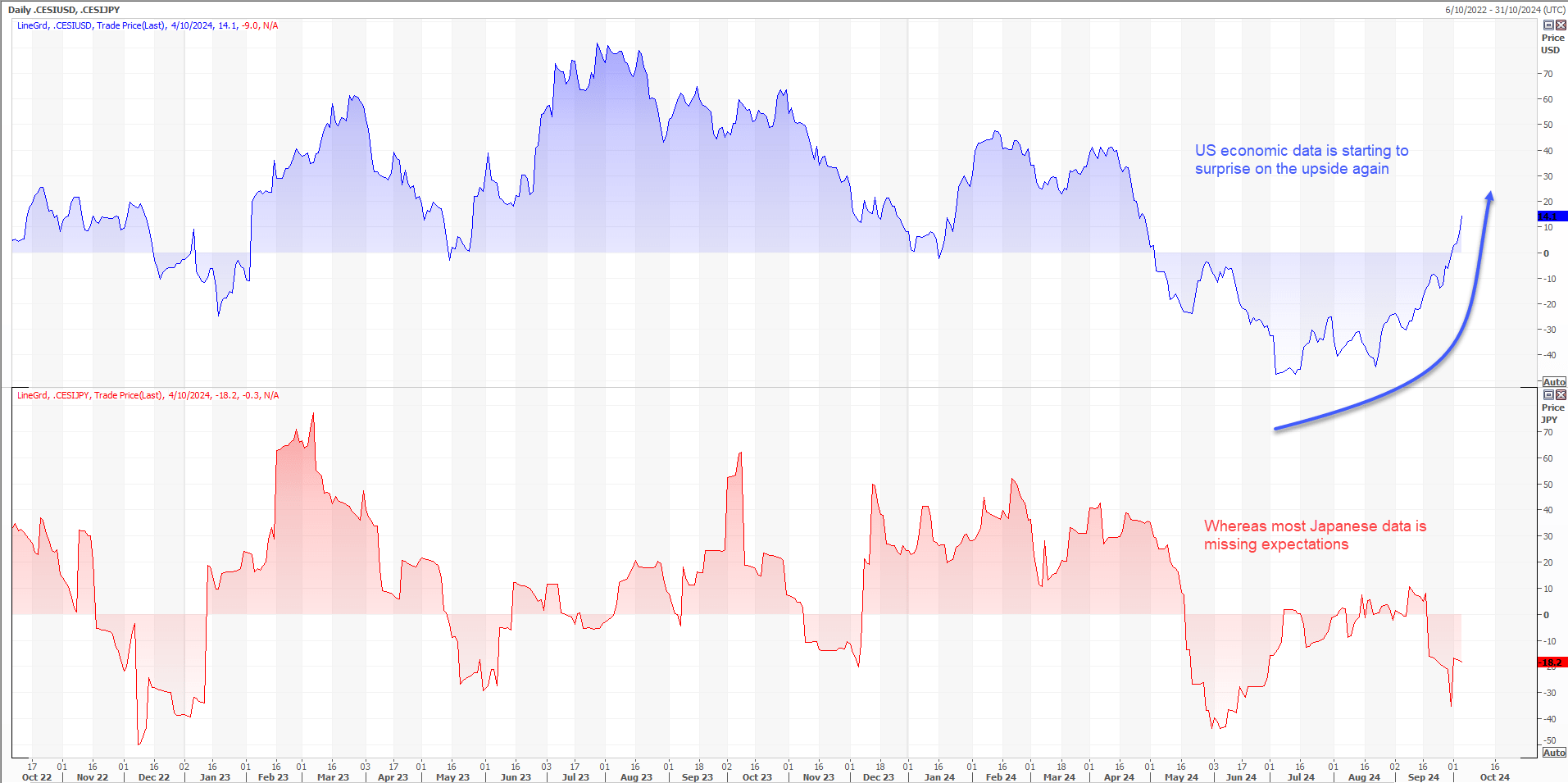

US economic exceptionalism returns

It’s not just the payrolls data that has impressed recently with Citi’s economic surprise index for the United States turning firmly higher over the past two months, moving into positive territory for the first time since early May. As an aggregate measure of how data prints relative to economist forecast, the positive figure indicates more data than not is now topping expectations. In contrast, Japanese data often undershoots, helping to shift the expected interest rate outlook for both nations.

The US outlook is becoming less dovish while Japan’s is turning less hawkish. That’s important for USD/JPY, especially the US side of the equation, given how influential it continues to be when it comes to directional risks.

Source: Refinitiv

Which is powering USD/JPY reversal

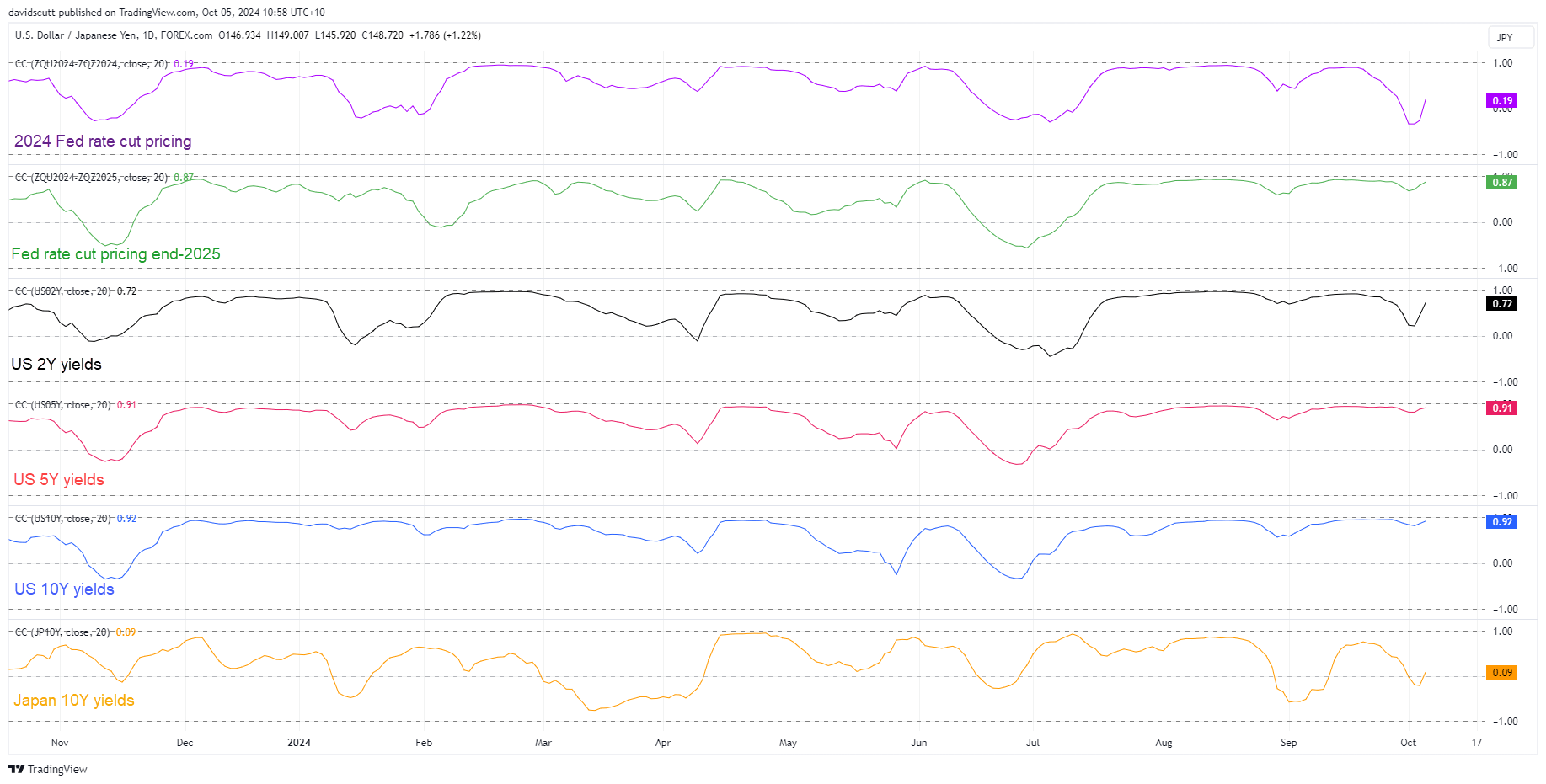

The following chart looks at the rolling daily correlation between USD/JPY with a variety of financial variables over the past four weeks, giving us a sense as to what’s influencing its movements.

From top to bottom we have 2024 Fed rate cut pricing, Fed rate cut pricing out to end-2025, US two-year yields, US five-year yields, US 10-year yields and Japanese 10-year yields.

As a reminder, correlation coefficient scores range from 1 to -1. The closer to either of those figures, the stronger the positive or inverse relationship between the two. A score of 1 indicates that both move in lockstep with each other.

You can tell the US interest rate outlook is incredibly influential on USD/JPY movements, especially Fed rate cut pricing over the next 15 months and US bond yields five-years out and longer. The 0.09 correlation coefficient score it has with Japanese 10-year bond yields suggests there’s almost no relationship, underlining that it’s the US rate outlook you should care about, not Japan’s.

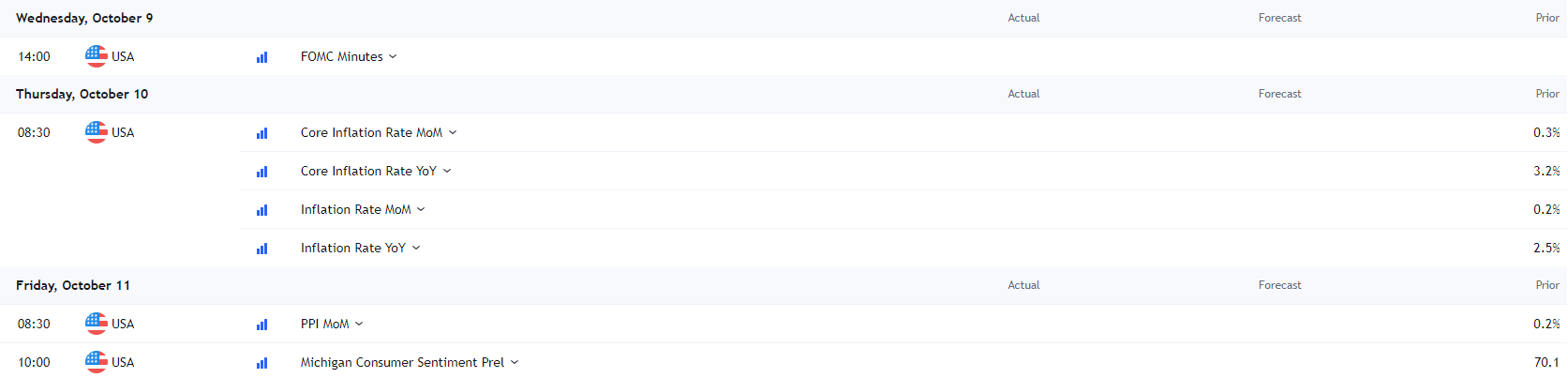

Key event risks ahead

Armed with that knowledge, it becomes an easy task to determine what events are important for USD/JPY and those that are not. We need to care about what Fed officials are thinking regarding the rates outlook as they’re the ones who determine it, so here’s the known speaking schedule next week. All times US EDT.

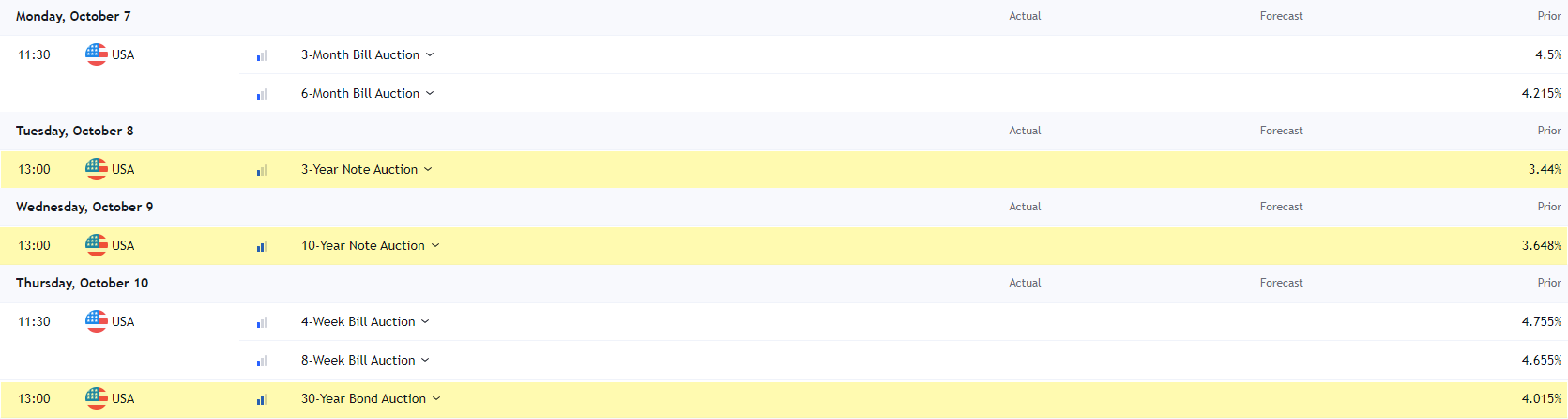

With the US rate outlook less certain due to strength in recent data, upcoming Treasury auctions of three and 10-year notes on Tuesday and Wednesday respectively, and 30-year bonds on Thursday, should be on the radar for signs of shifting demand which may impact yields significantly.

The US data calendar is also important with consumer and producer price inflation figures for September released on Thursday and Friday respectively. Both topped expectations in August, and with concerns about the labour market outlook subsiding, further heat could rekindle inflationary concerns. Once is an anomaly, twice is a trend, as the saying goes.

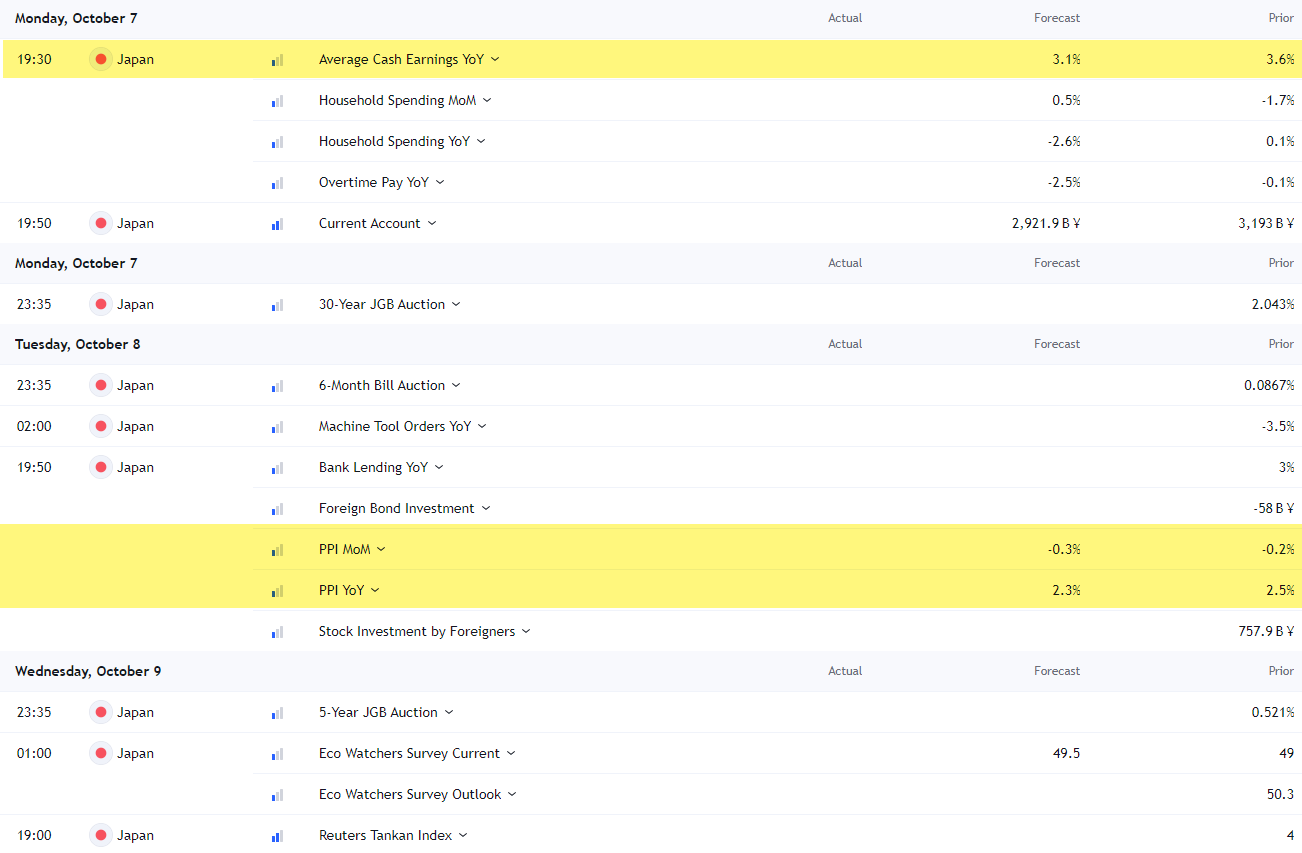

While Japanese data should be regarded as a distant secondary consideration when it comes to USD/JPY movements, there are some notable releases coming up this week. Those that may generate short-term volatility are highlighted, such as cash earnings and PPI. The others, including household spending, have traditionally had little impact on USD/JPY.

Outside known events, the Middle East conflict has to potential to override the US rates outlook as the primary market driver of USD/JPY next week, with a major escalation or de-escalation likely to generate downside and upside risks respectively. Movements in the offshore Chinese yuan against the US dollar (USD/CNH) may also be worth watching as it has often been highly correlated with USD/JPY at times in recent years, even if not so currently.

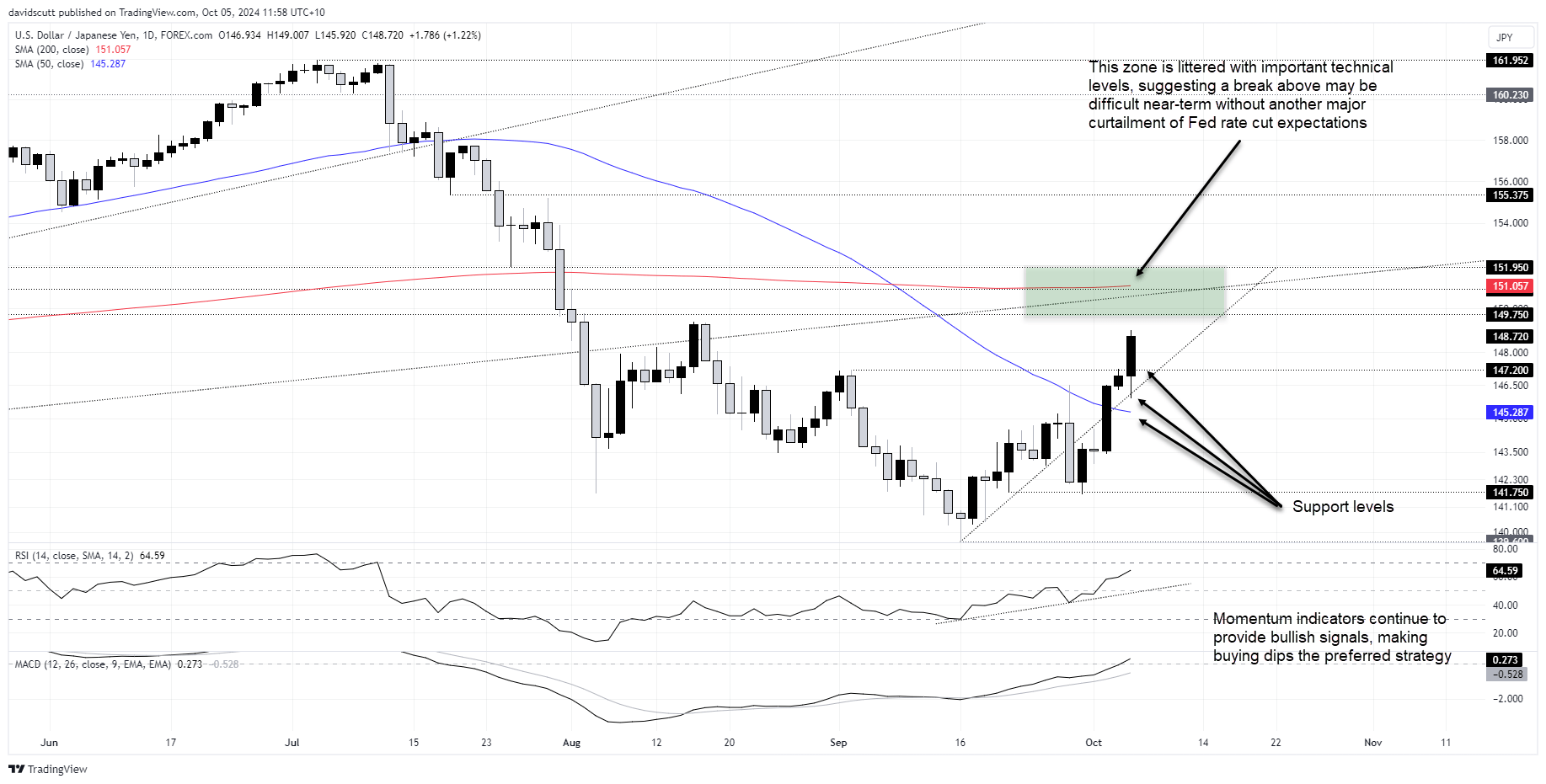

USD/JPY rebound facing far tougher technical tests

Last week comes across as a game-changer for USD/JPY heading towards year-end, sending it careening back above the 50-day moving average, an important development that could influence directional risks beyond the short-term.

The bounce off uptrend support on Friday saw the price take out horizontal resistance located at 147.20, suggesting that level may now act as support should we see any pullbacks this week. Along with the 50-day moving average, they’re the downside levels to consider when contemplating potential trade setups.

On the topside, 149.75 is an important level having acted as both support and resistance on numerous occasions this year and last. Above, we have a number of other key levels such as former uptrend support, 150.90 which acted as support and resistance on multiple occasions earlier this year, along with the 200-day moving average.

Unless we see another major curtailment of Fed rate cut pricing, the probability of breaking above this resistance zone comes across as unlikely near-term, suggesting the easy money from long trades has already been made. With MACD and RSI (14) providing bullish signals on momentum, the bias is to buy dips given the likelihood of range trading.

-- Written by David Scutt

Follow David on Twitter @scutty

Latest market news

Yesterday 11:06 PM

Yesterday 01:00 PM

November 30, 2024 12:00 PM

November 29, 2024 05:53 PM

Latest articles

Yesterday 11:06 PM

November 30, 2024 12:00 PM

November 29, 2024 01:55 AM

November 29, 2024 01:11 AM