January 26, 2022 11:23 PM

Headline consumer prices rose by 1.4% q/q, taking the annual inflation rate to 5.9%, up from 4.9% in the September quarter. As expected, Covid disruptions, strong commodity prices, and wider global inflation contributed to a significant lift in tradable (imported) inflation (+6.9%).

Elsewhere, gains in non-tradable or domestic inflation were especially strong driven by increases in construction prices, labour shortages, and transport costs.

Non-tradable inflation represents over half of all the items in the CPI basket. With little ability to influence tradables or imported inflation, the RBNZ will be aiming to slow down non-tradable inflation with rate hikes.

The RBNZ lifted the overnight cash rate twice in 2021 to 0.75%. As inflation is now almost twice the top of the RBNZ’s target band, there is little in the way to stop the RBNZ from lifting the overnight cash rate back to neutral at 2.5% by mid-2023.

Despite the higher inflation number and expectation of future RBNZ rate hikes, the NZDUSD has been taken hostage by this morning’s FOMC event, which has resulted in a solid bout of risk aversion across regional equity markets.

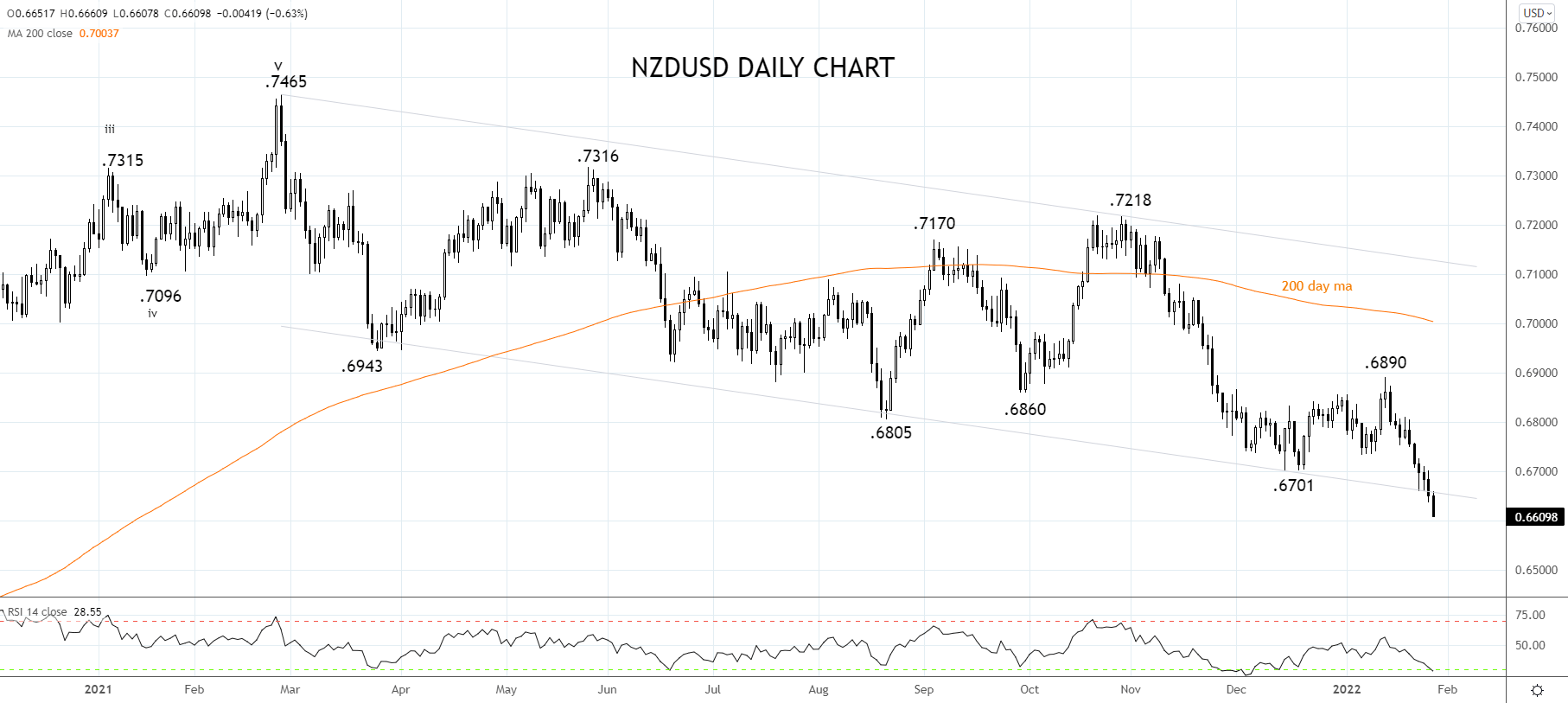

The chart below shows that the NZDUSD has broken below the multi-month trend channel support noted earlier in the week at .6660/50. While below here, there is scope for the decline to extend towards .6550 and then to .6500c in the medium term.

Source Tradingview. The figures stated areas of January 27th, 2022. Past performance is not a reliable indicator of future performance. This report does not contain and is not to be taken as containing any financial product advice or financial product recommendation

Latest market news

Today 02:05 PM

Latest articles

August 17, 2022 03:43 AM

May 25, 2022 03:13 AM

May 24, 2022 07:02 AM

May 2, 2022 11:45 AM