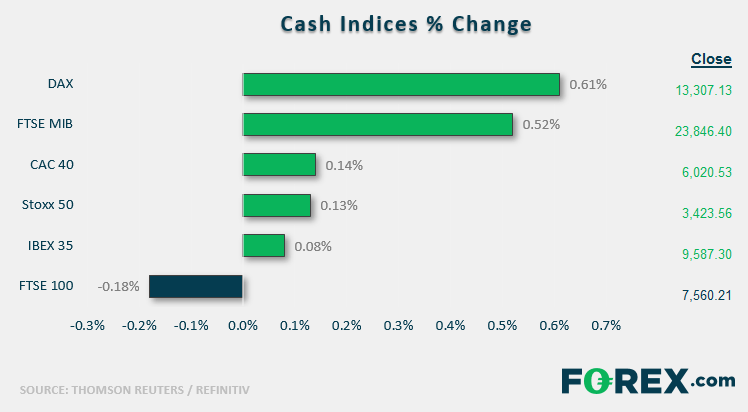

Stock market snapshot as of [8/1/2020 3:45 PM]

- The aftermath of fresh geopolitical drama is less thunderous for global markets than precipitating events

- EMEA indices have been slower to venture into the green than U.S. stocks, though all equity markets remain off lows

- Along the spectrum of ‘retaliation scenarios’ following the U.S. missile attack on one of Iran’s top generals last week, the one that Tehran instigated overnight should rank among the most restrained. Despite more than a dozen missiles reportedly fired on the Ayn al-Asad base in western Iraq and another in Erbil, there were no casualties. Tehran’s subsequent statement framed the move unequivocally, at least at the secular level: “proportionate measures” have been concluded, “we do not seek escalation or war”

- President Donald Trump’s tweeted conclusion that “All is well” was less convincing, but certainly flagged a reduced probability and imminence of escalation. The White House later signalled its interpretation of the attack as designed to satisfy retaliatory imperatives with the most minimal possible response, in order to avoid devastating U.S. counter assault

- Evidently, the view that recent Middle East events have fomented a tinder box, is still prevalent. Yet haven flows have abated considerably since news hit in early European hours. Tell-tale signs of ‘safety seeking’ remain in equity markets too. Select utility stocks see interest. Again though, caution hasn’t overshadowed interest in ‘riskier’ sectors like semiconductors in the wake of better-than forecast Samsung results

- For the near term, markets are likely to stage a second attempt at a gradual return to calm—albeit uneasy—as the one seen in the days following Qasem Soleimani’s death. The risk of continued escalation will continue to lurk in the background though investors are set to apply an increasing discount if Tehran and Washington signals that a line could soon be drawn under the specific matter of Soleimani’s assassination turn out to be correct. A press conference with Donald Trump has been scheduled for 16.00 GMT

Stocks/sectors on the move

- Another sign that European investors aren’t notching ongoing risk assessments at the most elevated levels: chip stocks are participating in sector cheer after Samsung’s better than expected earnings. Samsung’s biggest profit generator, enabled earnings to avoid the lowest forecasts

- Auto industry shares help Europe’s consumer sector into the green, led by Michelin, following a brokerage upgrade. The stock was up 2.2% into U.S. trading

- The weaker sectors were led by UK and French commercial property shares. This follows news that British Land’s proposal of a tower block in a central residential district was rejected. The stock fell 3%

- Boeing fell 1.7%. Grim exoneration is the most probable outcome after the latest tragedy involving a 737. The crash of a flight on its way to Ukraine from Iran involved a predecessor model of the 737 MAX. Boeing has accepted that flight control software known as MCAS played a key part in two fatal crashes between October 2018 and last March. MCAS was specifically developed for the 737 MAX

- Walgreens Boots Alliance tanks almost 7% as core drugstore profits slid in the first quarter, underscoring WBA’s reasons for looking into going private

- Lennar, the big homebuilder, rose 3.4% on better than forecast Q4 sales

- Costco will be the other large cap to help kick off earnings season when it reports after the U.S. close. Its stock traded 0.6% higher

- Macy’s holiday season trading report brought respite to turbulent retail shares after it noted a “strong trend improvement”. Kohl’s, Walmart, Target and Nordstrom were all higher. Macy’s rose 7%

- Beyond Meat and McDonald’s continue an uneasy association. The synthetic-food maker’s stock rose 4% on news that MCD will expand tests of BYND’s plant burger

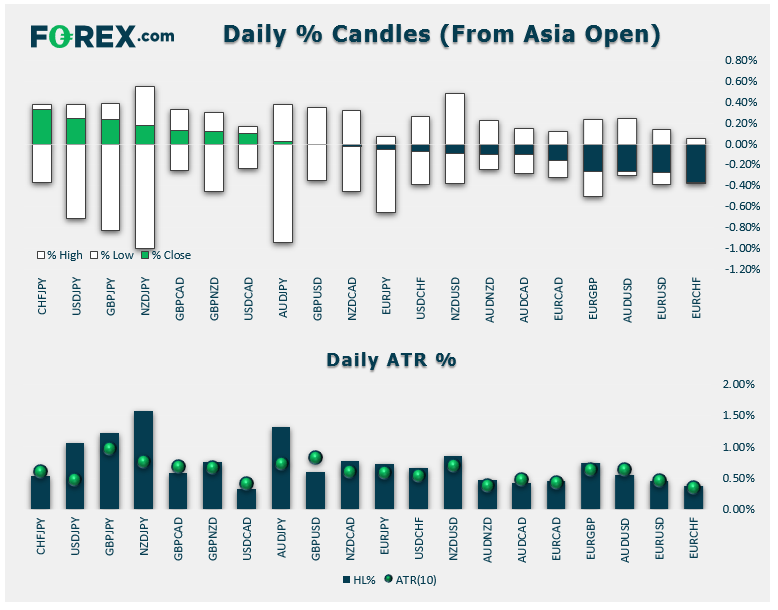

FX snapshot as of [8/1/2020 3:45 PM]

View our guide on how to interpret the FX Dashboard

FX markets

- Currency trading also reflects the rapid swing from ‘risk-off’ to ‘risk-on’ albeit of the most cautious kind. The dollar index saw losses of around two tenths of a percentage point before rising 0.1% as U.S. stock trading began

- The yen has given up earlier gains of as much as 0.7%. Suspected algo-drive trading had a field day earlier after a deluge of “Iran” and “attack” keywords hit the Twittersphere and beyond. Importers reportedly bought the USD/JPY dip below 108, adding momentum to the bounce

- G10 FX has generally adopted a wait-and-see stance, as pairs drift within 0.3% higher or lower on the day

- EUR/USD sees a 0.3% loss after another slab of soft data, namely an Ifo business sentiment reading and unimpressive German factory orders

Latest market news

Today 02:05 PM

Today 11:59 AM

Latest articles

November 2, 2023 01:41 PM

November 1, 2023 01:33 PM

October 31, 2023 01:15 PM

October 31, 2023 10:24 AM