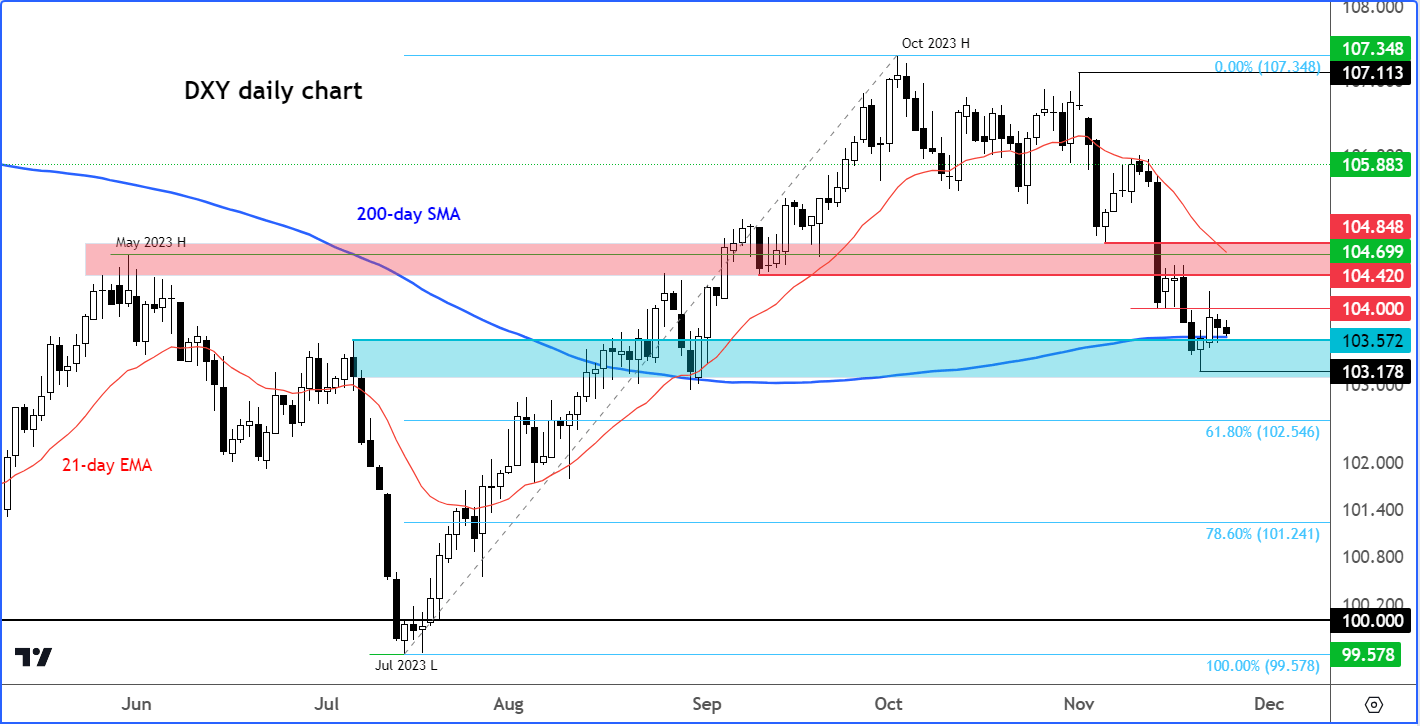

- US dollar analysis: Dollar Index bides time ahead of key data next week

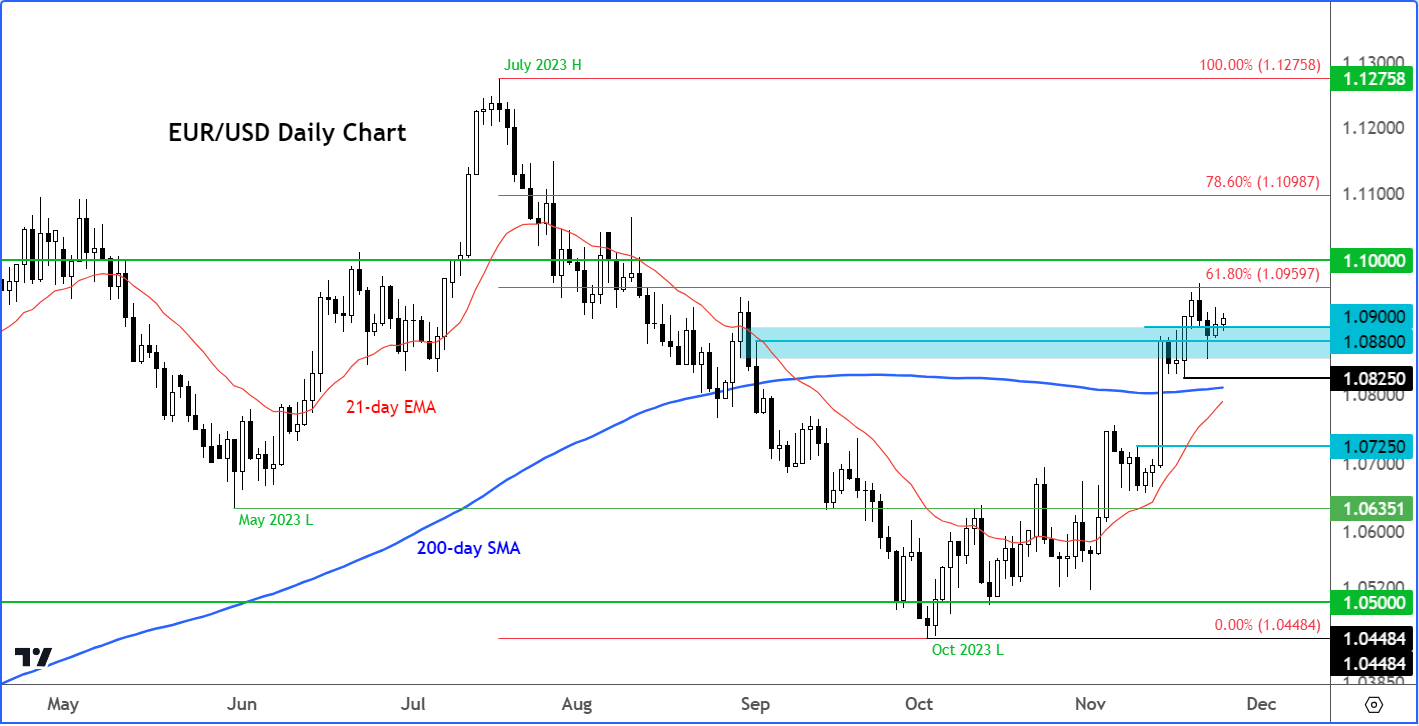

- EUR/USD analysis: Weaker Eurozone inflation data could paradoxically lift EUR/USD to 1.10

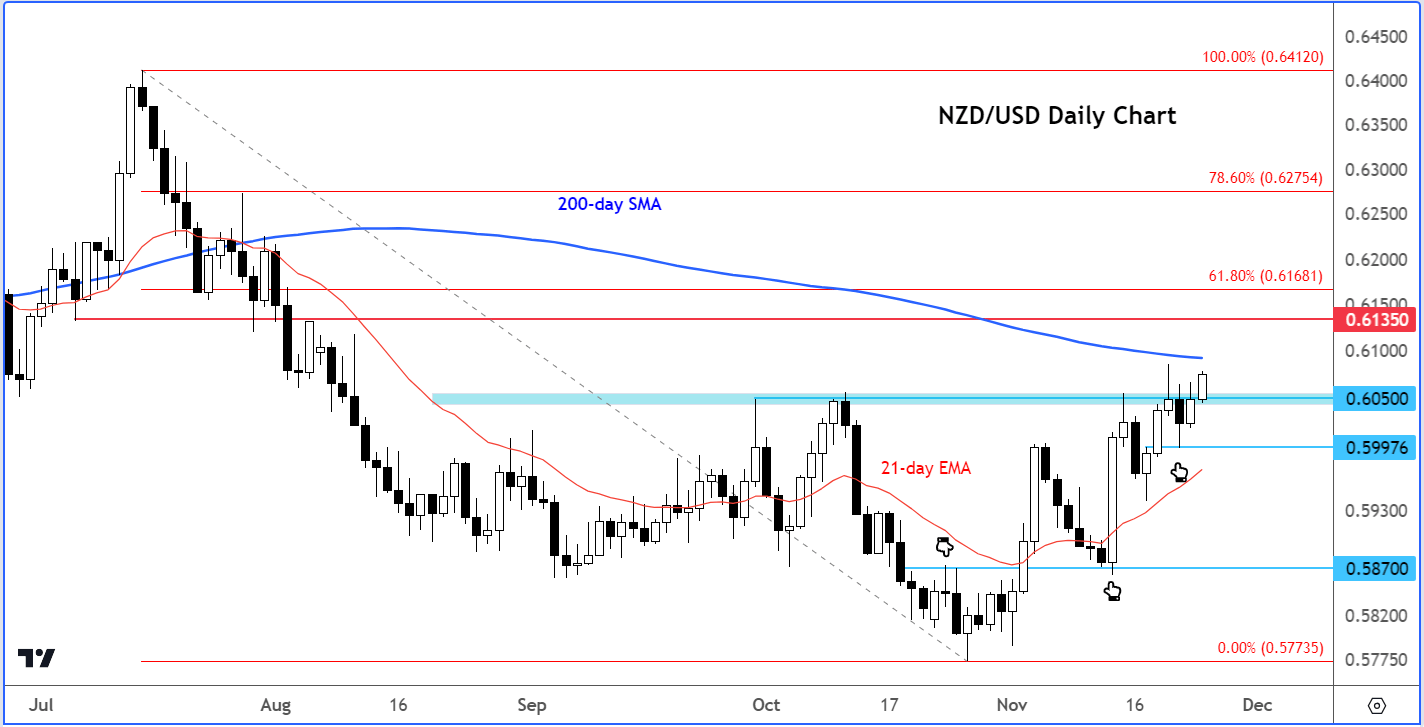

- NZD/USD analysis: kiwi looking bullish ahead of RBNZ rate decision

US dollar analysis: Dollar Index bides time ahead of key data next week

Following the sharp 1.9% drop in the Dollar Index last week, the DXY barely moved this week, partly because of a shortened week for US investors. But we also didn’t have much in the way of significantly important data to excite the markets. The FOMC minutes were overshadowed by last week’s soft CPI and PPI figures alongside rising jobless claims data. Together, these data releases poured cold water on recent hawkish Fed comments, keeping yields under pressure. This week, though, yields have been fairly stable like the dollar.

Clearly, market participants are watching data like hawks. But with global stock markets being excited by the possibility of central banks adopting a more dovish stance moving forward, with signs of global inflationary pressures slowly moving to normal levels, this should keep the dollar under pressure. I think the antipodean currencies have the potential to further make ground next week against the US dollar. The EUR/USD may also climb to the 1.10 handle.

US GDP and PCE inflation among next week’s US data highlights

The US GDP will be released on Wednesday, November 29 at 13:30 GMT. This will be the preliminary estimate of output for the third quarter, reported on an annualised basis (quarterly change x4). Despite its name, it is not the first estimate (i.e., advanced). Still, if we see a sharp revision from the 4.9% annualised print we saw in the initial estimate last month, this could move the markets. The initial estimate was higher than expected, and it caused a positive reaction in US dollar. Will we see a similar reaction this time, or are markets more focused on forward-looking data, given that GDP is now outdated by a good couple of months?

A day later, on Thursday, we will have the core PCE price index, due for release at 13:30 GMT on the day. Given that the US headline CPI readings fell below expectations, dampening the Federal Reserve's hawkish stance prior to the report, traders are now keen on observing a similar trend in the upcoming PCE inflation figures. This is crucial for them to maintain the belief that the Fed might reduce interest rates in the coming year. Core PCE is generally the Fed's preferred inflation metric due to its lower volatility compared to traditional CPI measures. Therefore, if this comes out stronger, it could negatively impact risk appetite, bolster the US dollar, and prompt traders to reconsider expectations of a sooner-than-expected rate cut in 2024. We think that a +0.2% reading or lower would align with the current market narrative of a peak interest rates and a potential rate cut in the first half of 2024. If so, this will likely weaken the US dollar and support risk assets.

EUR/USD analysis: Weaker Eurozone inflation data could paradoxically lift EUR/USD to 1.10

The EUR/USD was flattish in the first half of Friday’s session. ECB President Christine Lagarde said that the central bank has already done a lot on rates, and now they can afford to sit back and observe the impact of its past tightening. This suggests that the ECB is also done with rate hikes but may keep policy tight for a long period of time, until it becomes clear that the fight against inflation is well and truly won.

We will have the latest inflation data from Germany on Wednesday, followed a day later by the Eurozone flash CPI estimate. The latter eased to 4.2% annual rate in September from 4.5% the month before, following an even steeper fall the month prior. Let’s see if the trend of disinflationary pressures continued in October. If so, this should further boost the European stock markets, and thereby provide indirect support to the risk-sensitive euro.

Discouraging the ECB from tightening its belt further has been consistent weakness in Eurozone data. This morning from Germany, the November Ifo business climate index came in at 87.3 vs 87.5 expected. But the day before, we had slightly better-than-expected Eurozone PMI data, albeit both the services and especially the manufacturing sectors remained comfortably below the expansion threshold of 50.0, held back by French and German factories.

Paradoxically, the EUR/USD could push further higher if Eurozone inflation weakens more, since this will likely further raise the appetite for European stocks and provide indirect support to the risk-sensitive euro. Thus, a run towards 1.10 handle on the EUR/USD remains likely.

NZD/USD analysis: kiwi looking bullish ahead of RBNZ rate decision

The Reserve Bank of New Zealand’s rate decision is on Wednesday at 01:00 GMT. The RBNZ held interest rates unchanged for the third consecutive time at 5.5% as expected at its October monetary policy meeting. The last policy change was a 25-basis point hike back in May. Since then, the RBNZ has progressively gotten dovish, and it has more or less signalled that the tightening cycle is over. Past rate hikes have cooled economic activity and reduced inflation “as required.” But the RBNZ will keep its policy restrictive to ensure that inflation falls back within its 1%-3% target range. If there are no indications of policy loosening in the months ahead, then this might keep the NZD supported.

The NZD/USD has been finding support from broken resistance levels as shown on the chart, making higher lows. The key support that needs to be defended moving forward is around 0.6050, which was significant resistance in the past.

Source for all charts used in this article: TradingView.com

-- Written by Fawad Razaqzada, Market Analyst

Follow Fawad on Twitter @Trader_F_R

Latest market news

Today 02:05 PM

Today 11:59 AM

Latest articles

November 29, 2024 12:43 PM

November 22, 2024 12:51 PM

November 13, 2024 01:03 AM

November 8, 2024 02:15 PM