Six years to the day after ECB President Mario Draghi vowed to do “whatever it takes” to preserve the euro, the currency union is doing is certainly on stronger footing than it was then.

Indeed, it has been awhile since there’s been an ECB meeting with so little fanfare, with the central bank already outlining its tapering strategy and noting that interest rates would remain at current levels “through the summer” of 2019. With inflation running at 2% (but core inflation rising at just 0.9%), there’s certainly no urgency to raise interest rates any time soon.

As we see it, there are two key issues that investors will be watching at tomorrow’s meeting:

1) More clarity on “through the summer”

The aforementioned phrase has arguably muddied the waters more than it’s helped clarify the ECB’s plan, with some governing council members implying that interest rates could rise as early as June, others hinting that September was the sweet spot, and still others indicating a timeline even later. This “debate,” which could well continue for the next year, is why central banks usually avoid pre-committing to a specific monetary policy path in advance.

Having let the cat out of the bag last month though, Draghi and Company may seek to clarify the currently anticipated timeline while also emphasizing that it remains dependent on incoming economic data. Needless to say, any comments that suggest a rate increase could be in play earlier than market expectations (currently centered around September/October 2019) would be a bullish development for the euro, while a more conservative timeline could embolden euro bears.

2) Potential for “Operation Twist”

For readers who aren’t well-versed in the minutia of monetary policy (i.e. most sane people), “Operation Twist” was a strategy that the Federal Reserve employed in both 1961 and 2011 in an effort to keep long-term interest rates low and reduce borrowing costs without increasing its balance sheet.

In essence, the central bank could look to sell short-term bonds (where interest rates are anchored by a low policy rate) and replace them with an equal amount of longer-term bonds (keeping those yields subdued). When the Federal Reserve utilized this technique in 2011-12, the 10-year bond yield dropped to record lows below 1.5% while short-term rates held relatively steady.

So what does all that mean for markets? To the extent such a strategy would allow the ECB to keep its policy rate lower for longer, any indication that such a policy could be on the table would be a bearish development for the euro.

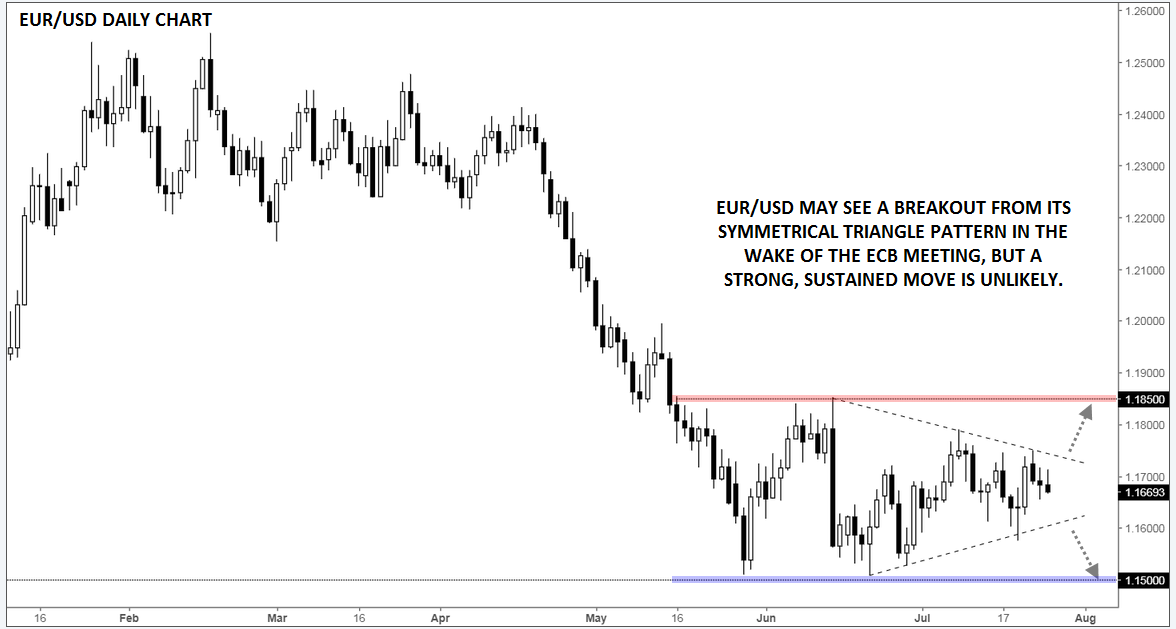

Technical View: EUR/USD

Speaking of the single currency, EUR/USD is poised for a breakout, with rates consolidating in a symmetrical triangle…within a sideways range between 1.1500 and 1.1850. With no immediate changes (or even distant changes) to monetary policy expected, the pair is likely to remain within its broader sideways range, though a breakout from the increasingly tight symmetrical triangle pattern is possible. A bullish triangle breakout could open the door for a continuation up toward 1.1850 resistance, whereas a bearish breakdown could expose the 1-year low near 1.1500.

Source: TradingView, FOREX.com

Latest market news

Today 02:05 PM

Today 11:59 AM

Latest articles

November 24, 2024 03:00 AM

November 21, 2024 04:02 PM

November 4, 2024 07:16 PM

October 28, 2024 02:49 PM