Chinese policymakers have cut stamp duty on stock market trades for the first time since 2008, announcing the policy move among a sweeping array of measures on Sunday designed to support the nation’s struggling equity market. Given the success stamp duty changes have had previously when it comes to stock market performance, the news may provide the catalyst to spark a meaningful reversal of the recent bearish trend.

Quick recap of the measures announced

China’s Ministry of Finance announced the amount of stamp duty charged would be halved to 0.05% starting from August 28, a move it said was designed to invigorate capital markets and boost investor confidence. The government also pledged to slow the pace of initial public offerings (IPOs) and lowered deposit requirements for margin trading, adding to a lengthening list of measures already announced to help stabilise market conditions.

China’s mixed track record for stock market interventions

China’s government has attempted to deliver desired policy and economic outcomes using the nation’s stock market in the past, resulting in a string of boom-bust cycles in the period since the GFC. In 2006, Chinese equities rallied around 300% in a little over a year before giving back most the gains in similarly quick fashion. Of note, an increase in stamp duty on stock trades was one of the catalysts that contributed to the market crash.

Separately, Chinese stocks more than doubled in under a year back in 2015, again assisted by a strong of policy measures to support equities. That too proved to be unsustainable, giving back most of the gains within the space of months.

Measures provide scope for a stock market bounce

While we may see a similar outcome on this occasion, especially when you consider how depressed valuations and investor sentiment is while household savings reportedly sits at the highest level on record, the weak macroenvironment in China does not bode well for corporate earnings, especially with economic activity in other major nations clearly slowing down. Without meaningful support measures to spur on activity in the real economy, it’s debatable whether these latest measures can deliver anything more than a short-term bounce from oversold conditions.

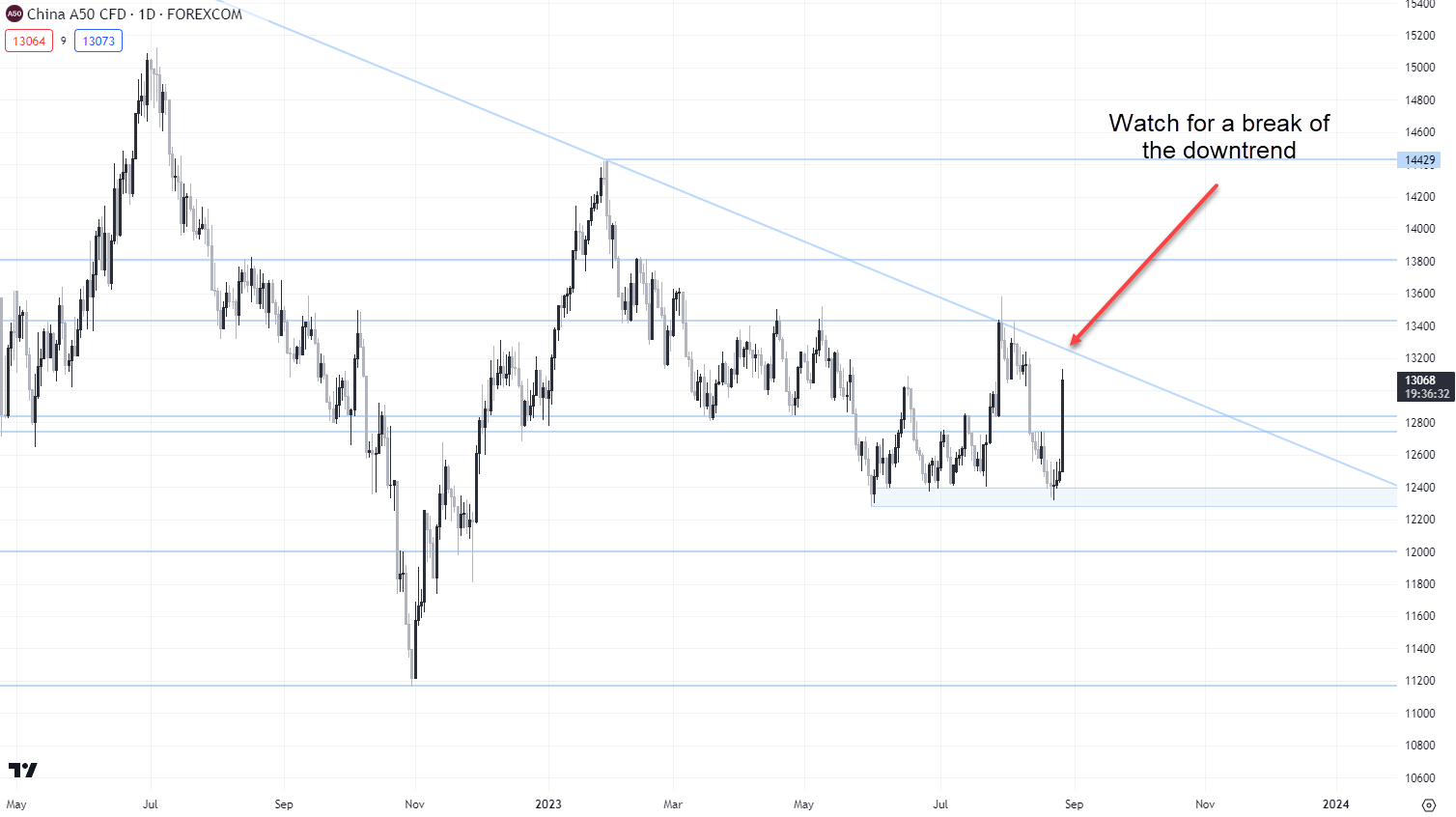

The China A50 looks set to rally hard on the back of the latest policy announcements, suggesting a retest of the strong downtrend it’s been stuck in could be on the cards. It currently kicks in around 13,260. A break of that level would open the door for a move back towards 13,400, 13,800 and potentially the year-to-date high located above 14,400. On the downside, support is likely to be found around 12,850 and again at 12,750.

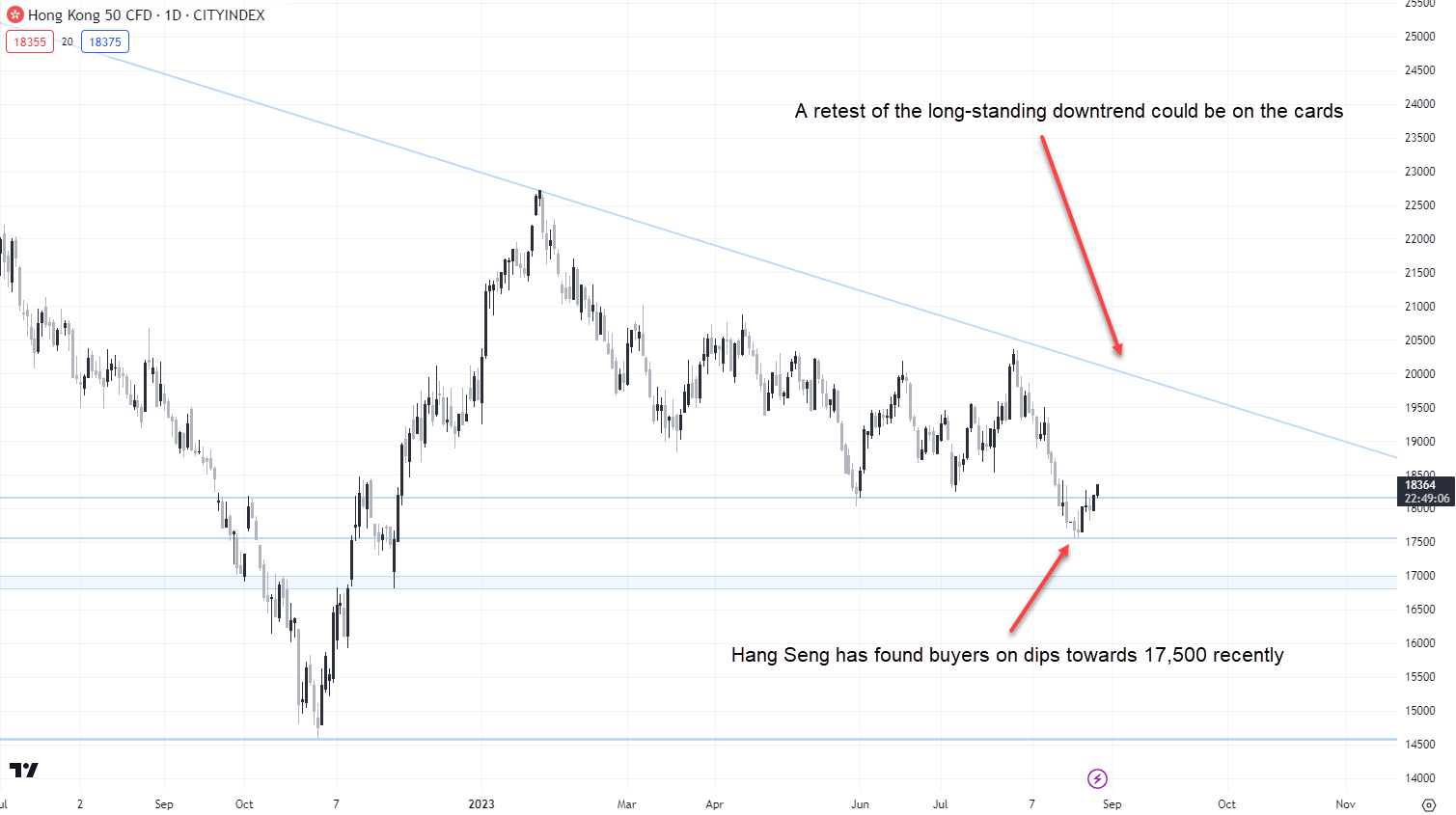

Like the A50, Hong Kong’s Hang Seng has found decent support recently, suggesting the latest policy measures may see a retest of the downtrend it’s been stuck in this year. Dips toward 17,500 have been bought over the past fortnight, suggesting a stop-loss order below that level may be appropriate for trades looking for a bounce. On the topside, there’s minor resistance located around 18,500, 19,000 and again at 19,500. The logical upside target will be a retest of the long-standing downtrend, currently located just above 21,000.

-- Written by David Scutt

Follow David on Twitter @scutty

Latest market news

Today 11:59 AM

Yesterday 11:06 PM

Yesterday 01:00 PM

November 30, 2024 12:00 PM

Latest articles

October 31, 2024 01:21 AM

October 21, 2024 12:56 AM

October 8, 2024 09:53 PM

October 2, 2024 06:47 PM