Market Brief Tariff Man strikes again

{kind=link}

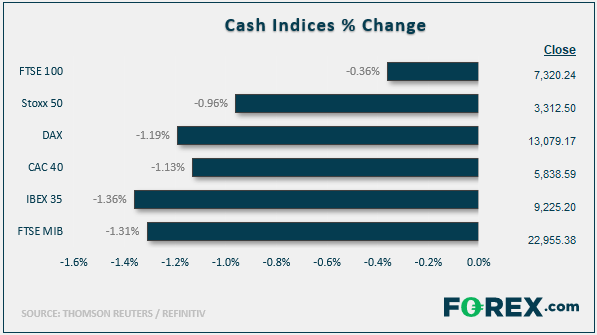

Stock market snapshot as of [2/12/2019 3:11 pm]

- Things were going quite well, then Trump tweeted. That’s a (somewhat facile) description of not just the first half of Monday’s global market proceedings, but apt for numerous sessions over the last 18 months or so. Monday may be a mild reminder that with global equities standing around cycle highs into the end of the year, whilst much remains inconclusive on trade, geopolitical and political fronts, tail risks may be higher than currently looks priced in

- Earlier, data from Caixin’s closely watched manufacturing PMI for China showed the sector growing for its first two-month stretch since the middle of 2018, and at the fastest rate of expansion for three years. Resilience in the world’s second-largest economy revives hopes of a base in its recent downturn. If corroborated it would have major implications for global markets into the New Year

- The official Chinese purchasing managers’ index, out over the weekend, also showed the sector returning to growth in November, boosted by a pick-up in production and new orders

- The DAX was among key European indices to benefit, albeit fleetingly

- After the U.S. President’s comments though, the German index slumped sharply, trading down 0.7% in the half hour before the U.S. cash open. Wall Street index futures retained a foothold in positive territory though were also markedly below the levels seen before the latest U.S. tariff news

Stocks/sectors on the move

- A mining and steel theme is inescapable and understandable after China's surprise manufacturing uptick and U.S. Presidential contributions. Hopes for a rebound in steel and base metal demand are being moderated after Trump tweeted that he would "restore the Tariffs on all Steel & Aluminum" from Brazil and Argentina

- BHP, Rio Tinto, Anglo American and Glencore were 0.7%-1% higher a short while ago, partly benefiting from positive brokerage commentary by RBC and Credit Suisse. These gains have been pared by Trump’s comments

- Fresnillo, the precious metals group, missed out on the day’s updraft entirely, dropping as much as 4% after lowering production guidance whilst raising capex expectations

- Newmont Gold Corp, the world's largest bullion producer by volume, also dropped production guidance whilst upping its 2020 cost outlook. It did however lower forecasts of its 2021/22 all-in sustaining costs. The trade slightly higher

- Ocado is a key UK standout. It slumps 7%-8% after surging higher by around double that rate on Friday. The online supermarket and technology platform has launched a convertible bond expiring in 2025. Institutions often hedge such bonds by shorting stock

{kind=link}

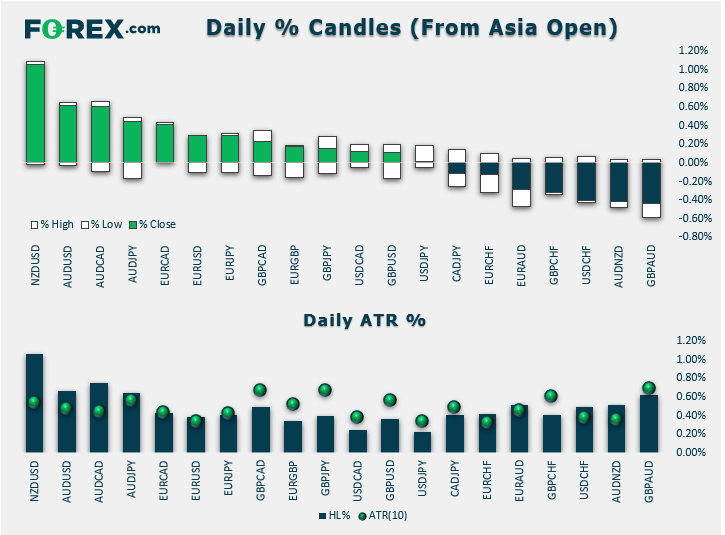

FX snapshot as of [2/12/2019 2:36 pm]

View our guide on how to interpret the FX Dashboard

FX markets including contributions from Senior Technical Analyst Fawad Razaqzada

- ‘Core’ fixed income markets have opted to discount some of Monday’s Trump factor, instead continuing to take their cue from promising global economic hints. Gold looks weak. As well as China’s manufacturing data, German factories posted a better than forecast showing in November, even if they still showed the sector was shrinking. Benchmark Eurozone bunds remain pressured as do U.S. Treasurys

- There’s little outright advantage for the dollar. DXY has slumped from 98.37 to 98.17 just now, as the quest for safety appears to ebb

- The Kiwi leads in the G10 amid a government spending pledge as commodity currencies see resilient flows in the wake of China’s indications

- The Canadian dollar is the weakest major on further signs that the BOC is preparing markets for a change of policy stance, if not outright rate policy changes, as early as its rate announcement scheduled for Wednesday

- The euro remains in familiar ranges albeit the single currency enjoys another positive session above $1.10. The move helps affirm last week’s 1.09812 intermediate low

- Elsewhere, the lira was steady as Turkey’s economy continued its gradual recovery from recession in the third quarter. GDP expanded by 0.9% following a contraction of 1.6% in the previous quarter, though the Q3 rise was lower than consensus

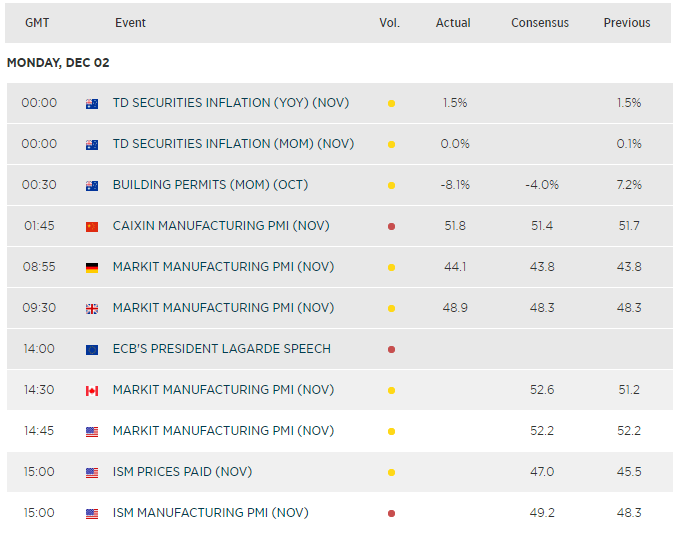

Upcoming economic highlights

{kind=link}

The information on this web site is not targeted at the general public of any particular country. It is not intended for distribution to residents in any country where such distribution or use would contravene any local law or regulatory requirement. The information and opinions in this report are for general information use only and are not intended as an offer or solicitation with respect to the purchase or sale of any currency or CFD contract. All opinions and information contained in this report are subject to change without notice. This report has been prepared without regard to the specific investment objectives, financial situation and needs of any particular recipient. Any references to historical price movements or levels is informational based on our analysis and we do not represent or warranty that any such movements or levels are likely to reoccur in the future. While the information contained herein was obtained from sources believed to be reliable, author does not guarantee its accuracy or completeness, nor does author assume any liability for any direct, indirect or consequential loss that may result from the reliance by any person upon any such information or opinions.

Futures, Options on Futures, Foreign Exchange and other leveraged products involves significant risk of loss and is not suitable for all investors. Losses can exceed your deposits. Increasing leverage increases risk. Spot Gold and Silver contracts are not subject to regulation under the U.S. Commodity Exchange Act. Contracts for Difference (CFDs) are not available for US residents. Before deciding to trade forex, commodity futures, or digital assets, you should carefully consider your financial objectives, level of experience and risk appetite. Any opinions, news, research, analyses, prices or other information contained herein is intended as general information about the subject matter covered and is provided with the understanding that we do not provide any investment, legal, or tax advice. You should consult with appropriate counsel or other advisors on all investment, legal, or tax matters. References to FOREX.com or GAIN Capital refer to StoneX Group Inc. and its subsidiaries. Please read Characteristics and Risks of Standardized Options.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

The products and services available to you at FOREX.com will depend on your location and on which of its regulated entities holds your account.

FOREX.com is a trading name of GAIN Global Markets Inc. which is authorized and regulated by the Cayman Islands Monetary Authority under the Securities Investment Business Law of the Cayman Islands (as revised) with License number 25033.

FOREX.com may, from time to time, offer payment processing services with respect to card deposits through StoneX Financial Ltd, Moor House First Floor, 120 London Wall, London, EC2Y 5ET.

GAIN Global Markets Inc. has its principal place of business at 30 Independence Blvd, Suite 300 (3rd floor), Warren, NJ 07059, USA., and is a wholly-owned subsidiary of StoneX Group Inc.

© FOREX.COM 2024